It was never about the house!

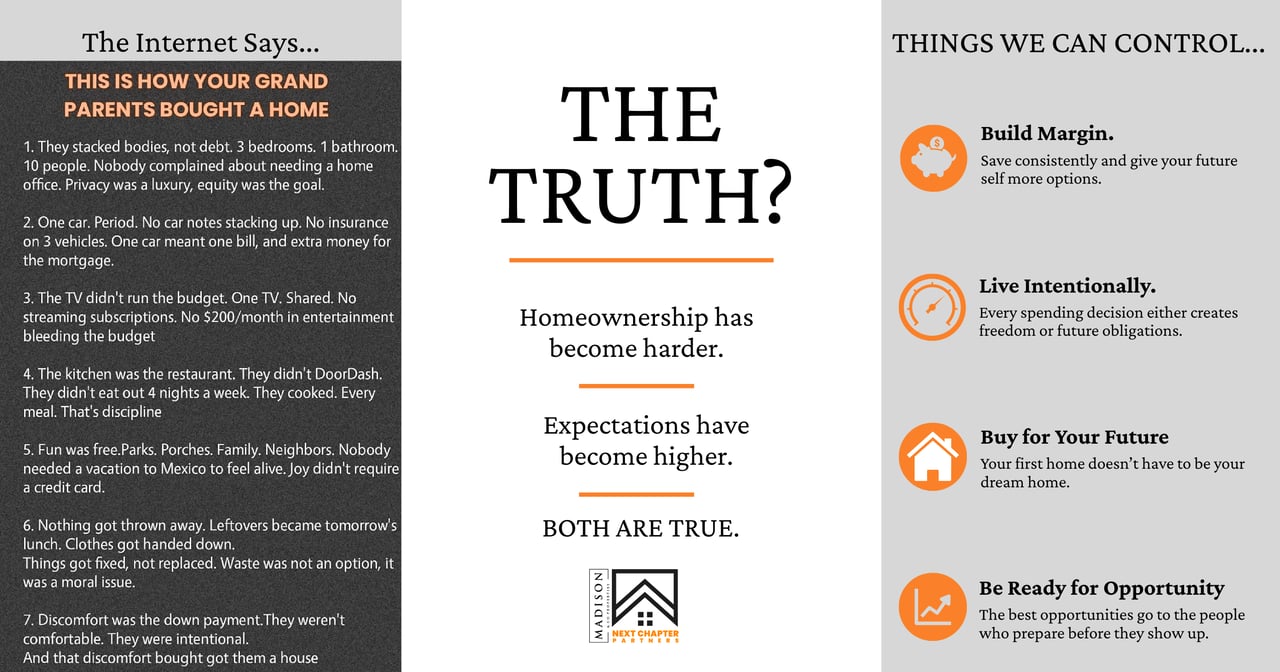

I saw this image, the one on the left, posted on social media today and there was far more controversy in the discussion than I expected. Our grandparents lived in smaller houses, drove one car, cooked dinner at home, fixed things instead of replacing them, and generally lived with a lot less. If people today would simply adopt those same habits, the argument goes, homeownership wouldn't seem so out of reach for so many.

In the comments, about half the people insisted previous generations simply worked harder and were willing to sacrifice. The other half argued that comparing today's housing market to the one our grandparents experienced is ridiculous. Homes cost a fraction of what they do today, wages stretched further, and college didn't leave most people carrying decades of debt.

As is often the case, both sides had valid points. However, neither side seemed interested in hearing the other's perspective.

There is no question buying a home has become more difficult. Home prices have increased faster than incomes in many parts of our country. Interest rates, student loans, and inflation all feed into this equation, too. None of these are realities that should be ignored.

However, at the same time, I don't think the original post was really about the housing market. That's at least not how it seemed to me. To me, it spoke to expectations and how much they've increased from one generation to the next.

Somewhere along the way, we somehow redefined what a first home is supposed to look like. A starter home was once exactly that - a place to start. Today, it's easy to convince ourselves that buying a home means finding THE home. It should have enough space for the family we hope to have one day, a dedicated office, updated finishes, a great backyard, and a neighborhood we will never outgrow.

There is nothing wrong with wanting those things because most of us want the same. The problem is that our expectations tend to grow much faster than our ability to pay for them. We don't notice it happening because it rarely occurs all at once. Instead, it happens one upgrade at a time. We buy a slightly nicer car because the payment fits our current budget. We commit to more subscriptions because each one is "only" a few dollars a month. We plan more elaborate vacations each year. And...we buy seek to buy homes that are just a little bigger, just a little nicer, and just a little more expensive than we originally planned.

None of those decisions, alone, are irresponsible. Collectively, however, they shape our financial future in ways we don't always recognize.

One of the biggest misconceptions I encounter is the believe that preparing to buy a home begins when you're ready to call a REALTOR (and by "a REALTOR, I mean me). In reality, it starts years prior to that point. It starts with building good financial habits before you have a specific reason to do so. It starts with keeping consumer debt under control, protecting your credit, saving consistently, and resisting the temptation to let every increase in income immediately become an increase in lifestyle.

Those habits don't guarantee homeownership, but they do something equally as important. They put you in a position to act when an opportunity presents itself. The same principle applies to investing.

I've had so many conversations with people who want to own rental properties someday, but haven't yet built the financial margin to take advantage of one if the right opportunity appeared tomorrow. They're waiting for the market to improve, for rates to come down, or for the perfect property to hit the market. Meanwhile, the things within their control often receive very little attention, if any.

Preparing for an opportunity has always been far more productive than waiting for one. I believe that is the lesson worth taking from our grandparents' generation. It's not that they had it easier or harder, but that many of them understood the value of creating margin. They didn't know what the future would hold any more than we do, but they built lives that left room to respond when circumstances changed.

The housing market will continue to evolve. Interest rates will rise and fall. Prices will eventually do what markets always do. Those are things that are beyond our control.

What remains within our control is whether we are building a financial life that creates options or one that slowly eliminates them. Homeownership, investing, and financial independence all become more attainable when we focus less on predicting the next opportunity and more on preparing ourselves to recognize it when it arrives.